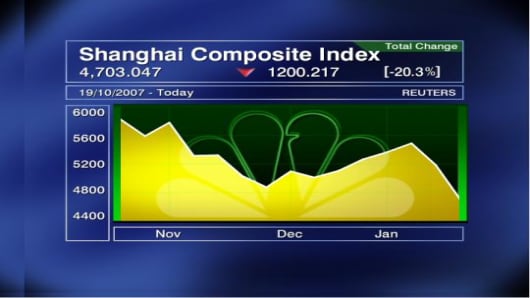

Asian markets closed sharply lower Wednesday with Japan losing over 3 percent lower and both Australia and South Korea ending around 2 percent down.

Selling intensified across the region after The Financial Times reported that KKR, the listed affiliate of private equity group Kohlberg Kravis Roberts, had begun a new round of talks with creditors and deferred repayment of debt due last Friday.

The KKR report added to investor worries about world economic health in view of rising oil prices that have prompted inflation fears. U.S. crude oil futures breached the $100 level on Tuesday.

Japan's Nikkei 225 Average slid more than 3 percent to its lowest close in a week, with the KKR report spooking investors into locking in profits. Sentiment had already been worsened by a fall in Sumitomo Realty & Development and other property shares, and selling of banks such as Sumitomo Mitsui Financial Group picked up in late trade.