It's like home buyers today are suffering from post-traumatic stress disorder.

The housing crash, foreclosure crisis and banking scandals have all combined to make buyers more sensitive than ever before.

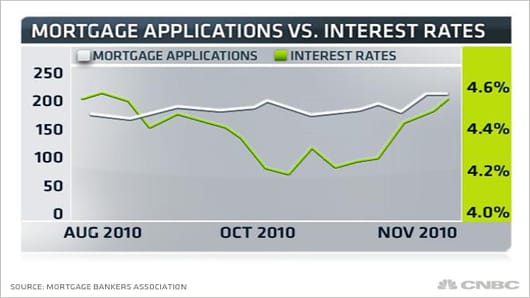

That's why the slightest fluctuation in mortgage interest rates have huge emotional power today.

"I think some people get a little fearful of what the higher payment might mean to them but they don’t' realize how minimal the difference might be," notes Eric Gates, President of Apex Home Loans in Rockville, MD.

In fact, Gates did a little math for me on the change in your monthly payment at different interest rates, if you buy a $200,000 home (just above the national median) with 20 percent down.

- 4.25%: $787.10

- 4.5%: $810.70

- 4.75%: $834.64

- 5.0%: $858.91

"Keep in mind that difference is mainly interest which is tax deductible. So, someone paying an extra $24 a month in interest who is in a 25% tax bracket is really only paying an extra $18 a month after the tax write off of the extra interest," Gates adds. Yes, cutting the mortgage interest deduction is currently being debated as a deficit-reducer, but the proposal is to reduce the cap from $1 million to $500,000, so it's not going to affect the buyers I'm using as an example here.