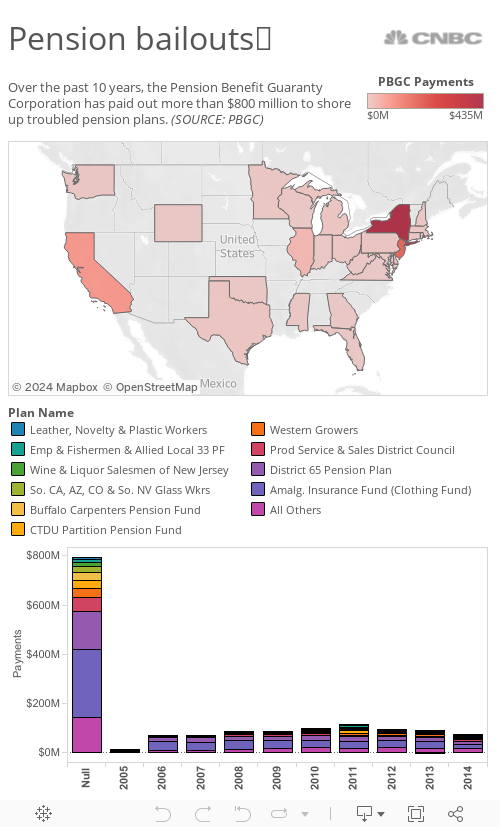

For many investors, last year's stock market gains helped make up for the heavy losses inflicted by the 2008 financial collapse. But it turned out to be a lousy year for private pension funds, which lost ground on their funding levels.

After gradual progress rebuilding the funds they need to pay retirees, the average private pension fund held about 80 percent of what it needs to cover those payments, according to a report by benefits consultant Towers Watson. That's down from 89 percent at the end of 2013 and represents an overall deficit among large corporate plans of about $343 billion, nearly double the shortfall a year earlier.