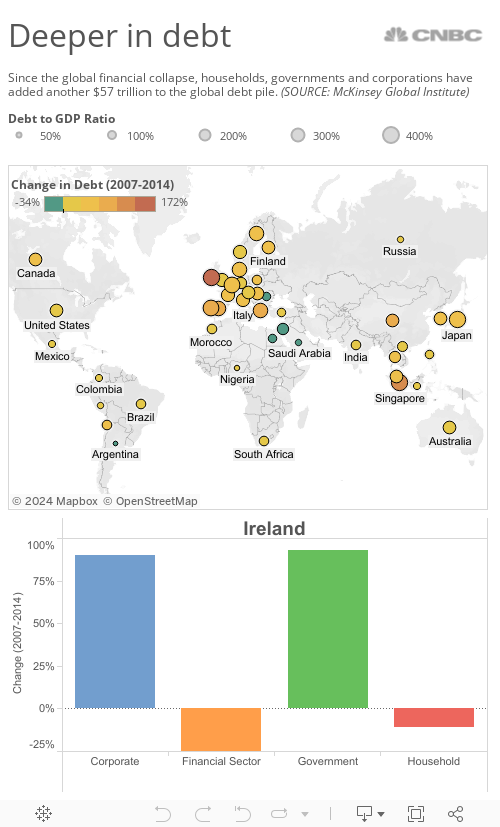

Despite widespread talk of "deleveraging" after a global credit bubble burst in 2008, the world continues to pile on more debt. According to a new study by McKinsey, the world ended last year some $57 trillion deeper in debt than it was in 2007.

The total tab—owed by governments, companies and households—is now more than twice the value of the world's total economic output.

The biggest chunk of new borrowing since 2007—some $25 trillion—has come from governments going deeper into hock. Of the nearly 50 countries included in the analysis, only five—Argentina, Egypt, Israel, Romania and Saudi Arabia—have paid down some of their debt.

Read MoreFinance ministers for Germany and Greece meet

For the U.S., McKinsey figures the total outstanding debt of all households, non-financial corporations, and government comes to about 233 percent of gross domestic product—which ended last year at $17.7 trillion. That works out to a total U.S. debt of a little more than $41 trillion.

Government was the source of that added borrowing (up 35 percent since 2007), while corporations pared debt by two percent and households cut back by 18 percent. U.S. banks shrank their total debt by 24 percent.