Signs of economic weakness and a global stock market sell-off have lowered the odds that the Federal Reserve will continue raising interest rates at its next regular meeting in mid-March.

But might the Fed reverse course and start cutting rates again? Not likely, according to an analysis by researchers at Oxford Economics of 30 years of policy decisions by central banks around the world.

Since the U.S. central bank embarked on rate "liftoff" in December — after nearly a decade of pushing rates to near zero — a global market sell-off and weak economic data have prompted many Fed watchers to predict the central bank will proceed slowly on its new path to higher rates.

Among policymakers, Fed "hawks" — who support raising the cost of borrowing to more "normal" levels — argue that an improved job market and a gradual rise in inflation validate the recent policy shift to boosting rates. Restoring rates to higher levels would also give central bankers more room to cut rates later if the U.S. economy slipped into another recession.

But other central bankers are leery of further rate increases, on the grounds that a slumping global economy is already creating a major headwind for the U.S.

One Friday, Fed Gov. Lael Brainard told a monetary policy conference in New York that economic weakness at home, along with "heightened spillovers" from abroad "could result in a lower policy path in the United States relative to what many had predicted."

Read More Fed's Brainard flags low rate future

Since December, market prices for federal funds interest rate futures — a bet on where the cost of overnight borrowing is headed — indicate that traders and investors agree that the central bank is likely to remain slow to boost rates this year.

Some Fed watchers have even suggested the central bank may have moved too quickly to hike rates and faces the prospect of easing policy again to spur economic growth.

"It's far more likely that they'll have to reverse themselves as a number of other countries have, like Sweden and others, where they raise the rates thinking it'll be fine and then have to drop it," University of Chicago economist Austan Goolsbee, a former Obama advisor, told CNBC last month.

Read MoreGoolsbee says Fed may cut rates in 2016

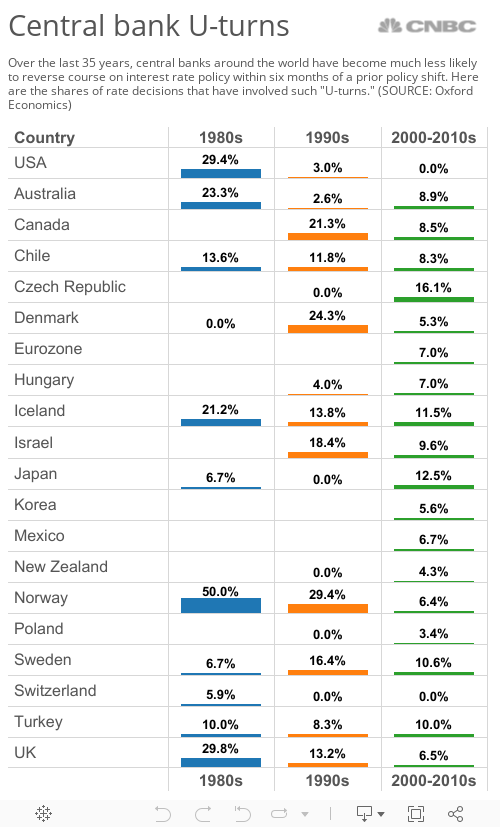

But if history is any guide, the odds are slim that the Fed will embark on a policy "U-turn" and reverse course within six months of a policy shift, according to the Oxford Economics analysis. Central bankers around the world, they found, have become far less likely to flip-flop on policy than they were 30 years ago.