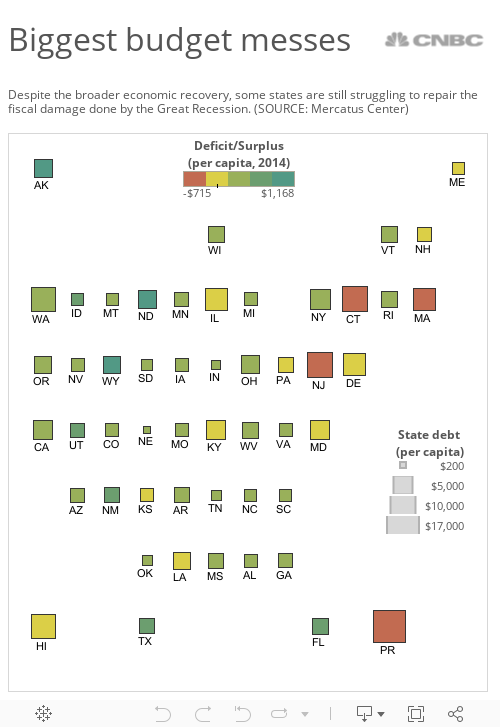

It's hard to imagine a state in worse financial shape than Illinois.

But three others face an even bigger fiscal mess, based on an analysis Wednesday from researchers at George Mason University.

Illinois lawmakers have set a pretty low bar. Late Tuesday, they failed in the latest, last-ditch effort to break a nearly yearlong stalemate that has left the nation's fifth-largest state without a budget. The relentless gridlock in Springfield has forced service cuts and threatens to close schools and colleges as the state enters a second year without a spending plan.

"We are like a banana republic," Republican Gov. Bruce Rauner told reporters late Tuesday after the latest budget standoff with the Democratic-controlled legislature. "We can't manage our money, and employers don't have any confidence in us. They won't come here unless we can get our act together and balance our budgets."

But as bad as things are in the Land of Lincoln, three other states are in worse fiscal shape, according to an analysis released Thursday by the Mercatus Center at George Mason University.

Connecticut, Massachusetts and New Jersey are coping with even bigger problems thanks to large accumulated debts, underfunded pensions and looming deficits, among other measures of fiscal health, the researchers found in an analysis of the latest state financial statements available.