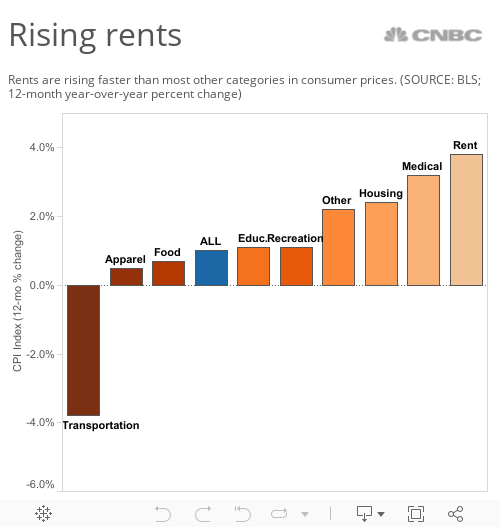

The cost of food, clothing and transportation has only been inching up slowly in the last year, helping American households make ends meet.

But for renters, the pressure on their paychecks keeps rising.

The latest sign came from the government's monthly report on the consumer price index, which breaks out the change in cost of major spending categories. Last month, for the second month in a row, the annual rise in rental income approached 4 percent, nearly four times the overall inflation rate of just 1 percent for the last 12 months.