If you've been holding out for your home's value to recoup the losses from the real estate bust, your wait might soon be over.

The recent rise in American incomes means households have more money to put toward buying a home, and households in some metro areas are seeing bigger increases than others.

That could translate into increased gains in home prices in many metro areas that have so far lagged the national price rises since the housing recovery began.

The latest read on American incomes came from a release of U.S. Census Bureau data this week, which showed that the median U.S. income rose by 5.2 percent last year, the first gain since the Great Recession sent unemployment soaring and left millions of households without paycheck.

Since then, the jobless rate has been cut in half, tightening the supply of qualified workers for new jobs and prompting employers to begin paying more to attract new hires and keep existing staffers from leaving.

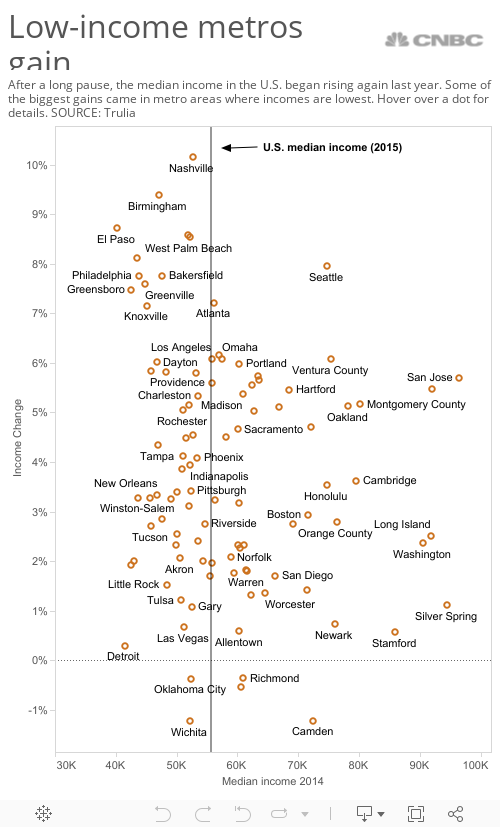

The single statistic for the national median income gain masks a wide range of income changes, including a marked difference from one metro area to another. Some of the biggest increases have come in cities where median incomes are lower than the 2015 national level of $56,500.

"Many of the metros that saw the highest income growth have been in places that have been slow to recover from the recession," said Trulia's chief economist, Ralph McLaughlin.