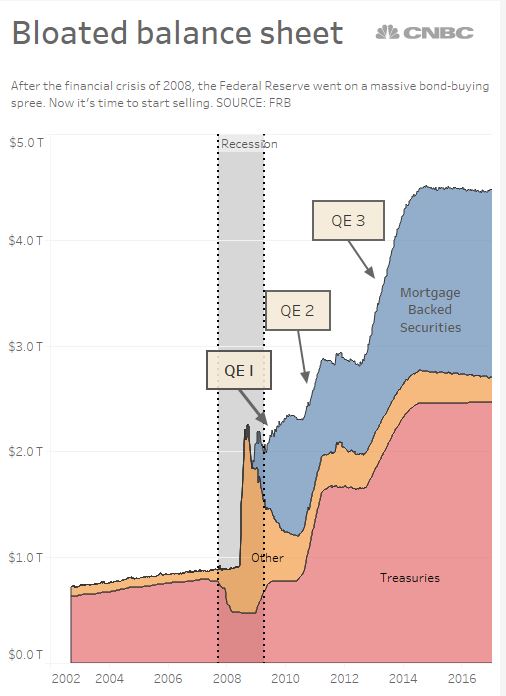

After the financial crisis of 2008, the Federal Reserve went on a massive bond-buying spree. Now it's time to start selling.

That means life has gotten more complicated for Fed watchers trying to second-guess what the central bank will do next.

Investors reading the tea leaves of Federal Reserve official pronouncements have long looked for clues about the policymakers' plans to raise or lower interest rates.

These days, they've got another mystery to ponder: the speed at which policymakers plan to shrink the size of the Fed's bloated balance sheet of $4.5 trillion in bond holdings.

Here's what you need to know to read along with the other Fed watchers peering into the central bankers' crystal ball.

So how did the Fed's balance sheet get bloated in the first place?

The initial surge followed the collapse of the credit markets in September 2008, after a wave of fraud swept through the mortgage market. Banks, investors and others were left holding hundreds of billions of dollars in worthless bonds backed by mortgages that were never going to be paid back.

To plug a giant hole in the financial system, the Federal Reserve pumped more than a trillion dollars into the banking system, as the economy slipped into what would be the deepest recession in decades.

The money infusion that followed the 2008 crisis was the biggest in the Fed's 103-year history, more than doubling the central bank's holdings of bonds and other securities virtually overnight. It was the financial equivalent of dropping cash from the sky, earning then Fed Chairman Ben Bernanke the nickname "Helicopter Ben."

Where did all that money come from?

When the Fed buys bonds in the open market, it pays with cash, which it, in effect, creates in the process. (It doesn't actually "print money" — that's the Treasury's job.) The extra supply of money lowers the cost of borrowing, also known as "monetary easing." The pace of bond buying in "open market operations" is set by the Federal Open Market Committee, or FOMC.

When the extra supply of money accelerates the pace of borrowing too far, the economy can start to "overheat," pushing inflation higher. That's typically when the FOMC reverses the money pump by selling some of its bonds, which drains cash out of the financial system (known as "monetary tightening.") The goal is to raise interest rates and cool things off.

So that 2008 infusion boosted the Fed's holdings to $2 trillion. Where did the other $2 trillion and change come from?

As the Great Recession deepened, the Fed embarked on several rounds of a controversial, never-tried policy to lower interest rates by buying even more bonds. To try to revive the housing market, the central bank spent heavily on mortgage-backed bonds in an effort to hold mortgage rates low and encourage homebuying.

Why buy all these bonds in the first place? Can't the Fed just lower rates directly?

The Fed has two main interest-rate levers. Shorter-term rates are set by changing the rates charged for big loans to banks on money they borrow and repay overnight to maintain the required level of cash reserves. After the financial crisis, when the Fed slashed that rate to near zero, the economy was still sliding in reverse. Because the Fed can't set short-term rates less than zero (the so-called "zero lower bound" in Fedspeak), it turned to an untested idea called Quantitative Easing, or QE, to push longer-term rates down to levels not seen in generations and hold them there indefinitely.

The policy involved buying bonds in the open market, using the Fed's credit, to create more money (or "liquidity"). All that extra money in the system reduced the cost of borrowing, but it left the Fed with a giant pile of bonds.

Did the QE plan work?

So far so good. The housing market has largely recovered, the stock market is setting new records and the unemployment rate is at multiyear lows. But it remains to be seen what happens next.

There are risks to holding on to all that debt and keeping interest rates so low indefinitely. One is that it discourages saving and encourages borrowing. Another is that all that extra money in the system could spark another round of inflation. (So far, inflation is historically very low.)

That extra money in the system could also create an "asset bubble." In fact, some critics of the Fed's massive bond-buying spree believe it has pumped up stock prices to unsustainable levels.

But there's also a risk of hurting the economy if the Fed sells off its bloated balance sheet too quickly. Just as buying up bonds pushed long-term interest rates lower, selling off those bonds too quickly would push rates higher. That would create a headwind for an already sluggish U.S. economy.

So what's the Fed's plan?

Given the uncertainties about the impact of the sell-off, the Fed plans to take baby steps, at least initially. After its June meeting, the FOMC unveiled a "normalization" plan that basically reduces its holdings gradually, based on a set of monthly reduction targets that start at $10 billion a month and rise over the next year to $50 billion a month.

That works out to about $600 billion a year, which means it would take roughly six years to sell off all the debt the Fed has bought up since 2008.

But shrinking the balance sheet that far would be a bad idea. That's because the economy and financial system has grown since 2008 and needs more money to continue operating smoothly.

It's not clear exactly when the Fed will decide its balance sheet is back to "normal." A lot depends on how well the economy responds to the upcoming shrinkage, and whether another recession forces the central bankers to reverse course.

Oxford Economics analyst Raymond Stone, after looking through the Fed's statements on the subject, estimates that if it keeps to the current schedule, the balance sheet will be back to "normal" in May 2021, when it hits a little less than $3 trillion.

But a lot can happen in the next four years.