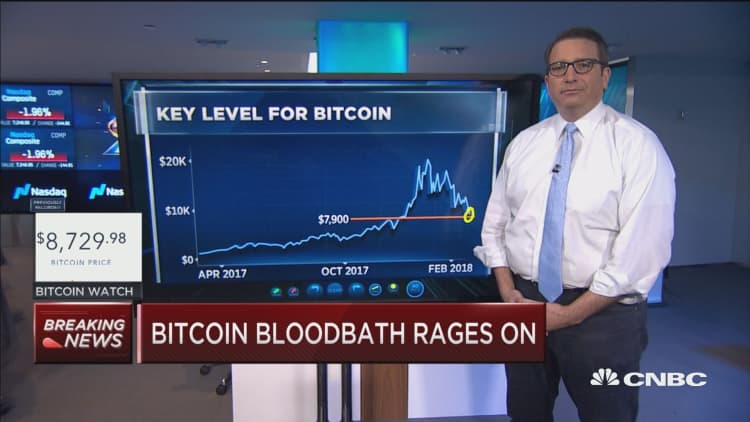

Bitcoin fell below $8,000 for the third time in four days on Monday amid a broader sell-off in cryptocurrencies that has seen over $60 billion of valued erased from the market in 24 hours.

The price of bitcoin traded as low as $7,178.65 on Monday and sat below the $8,000 mark for most of the morning's trade, according to CoinDesk. It's the lowest price for bitcoin since November 16. CoinDesk's bitcoin price index tracks prices from digital currency exchanges Bitstamp, Coinbase, itBit and Bitfinex.

On Friday, bitcoin fell below $8,000 for the first time since November 24. It then rose above $9,000 over the weekend before falling below $8,000 on Sunday.

It was not only bitcoin that fell either. Other major virtual currencies, including ethereum and ripple, fell sharply in the last 24 hours. The market capitalization or value of the entire cryptocurrency market fell to around $350 billion around 11:23 a.m., ET, Monday, according to data from CoinMarketCap.com. This was a drop of around $67.7 billion in 24 hours.

Threats from China and India

The digital currency world has been plagued by a string of worrying headlines. Tougher regulation has been a key factor weighing on price.

On Monday, Financial News, a publication closely affiliated with the People's Bank of China, reported that the central bank will block all platforms related to cryptocurrency trading and the issuance of so-called initial coin offerings (ICOs). Previously it had stamped out domestic cryptocurrency exchanges but it extended its crackdown to foreign platforms too.

"In the future, any related (platform) will be closed as soon as it is found. At the same time, further regulatory measures will be taken with the future development of the situation," the Financial News reported.

India's Finance Minister Arun Jaitley said last week that the country wants to "eliminate" the use of digital currencies, though India is a minor player in cryptocurrencies and the government apparently has yet to act.

Banks: Forget using credit cards to buy crypto

Major banks are also starting to curb the use of their services to buy cryptocurrencies. On Monday, major U.K. lender Lloyds Banking Group said that it was stopping people buying cryptocurrencies using credit cards. The move follows U.S. banks J.P. Morgan Chase, Bank of America and Citigroup, who implemented the same policy last week.

Other worries are plaguing the digital currency market, particularly around a cryptocurrency called tether. Some experts have suggested that tether, which is pegged to the U.S. dollar, could be being created to prop up the bitcoin price.

$100,000 bitcoin ahead?

Still, there are bullish voices in the market.

Fundstrat's Tom Lee, the only major Wall Street strategist to issue formal price targets on bitcoin, said in January that $9,000 is a "major low" for bitcoin and "the biggest buying opportunity in 2018."

Lee issued another report last week that maintained his $25,000 price target for bitcoin.

And Kay Van-Petersen, a Saxo Bank analyst who correctly predicted the cryptocurrency's rally at the start of 2017, told CNBC recently that bitcoin could hit between $50,000 and $100,000 this year.