As small business owners recover from the pandemic, it's important to make sure they get their personal and business finances back on track, said personal finance expert and best-selling author Suze Orman.

That includes saving, investing and managing credit card debt.

"You have got to put yourself in a situation that no matter what happens, you can pay your bills," said Orman, host of the podcast, "Women & Money (And Everyone Smart Enough To Listen)."

Orman shared her advice and much more to LGBTQ+ small business owners and allies during CNBC + Acorns Invest in Pride: Ready. Set. Grow. on LinkedIn Thursday.

Here's how Orman suggests small business owners tackle their money as they move forward post-pandemic.

Retirement planning

There are several options for small business owners to save for retirement.

They can open a SIMPLE IRA, which allows employees to contribute money to the plan, or a SEP IRA, in which only the owners can make contributions. They can also fund a solo 401(k), which covers a business owner with no employees.

More from Invest in You:

Suze Orman likes bitcoin. Here's how she says you should invest

How these small businesses pivoted to survive during Covid

Here's how to decide what debt you should tackle first

Sole proprietor James Kingman, psychotherapist and owner of Atlanta-based Unlimited Spectrum Counseling, wanted to know how to get started.

Orman's advice: Since he doesn't have employees, he should contribute to a Roth IRA until it is maxed out (which is $6,000, or $7,000 if you are over 50 in 2021). Then, open a solo Roth 401(k).

Once Kingman has employees, look into other alternatives, Orman said.

Start young

The earlier you start saving for retirement the better because of compound interest, which is interest earned on interest.

"It is like a little snowball rolling down a mountain in beautiful snow and it gets bigger and bigger and the longer it rolls, the bigger it gets," explained Orman, who recently co-founded Secure, an employer-matched emergency fund for employees.

For instance, if an 18 year-old opens a Roth IRA and contributes $100 a month for the next 40 years, assuming a 12% annual average rate of return, he or she would end up with $1 million. If he or she waited 10 years to start, the end result would be only $300,000 by age 58, she said.

Non-retirement savings

An emergency savings of 12 months' worth of expenses is a must these days, Orman said.

If you want to save more after that, outside of a retirement plan, a series I savings bond is a fabulous investment if you have at least up to $10,000, she said. It's tied to inflation, which has been rising.

The interest rate is a combination of a fixed rate, currently 0%, and a semiannual inflation rate, currently 3.54%.

It has a minimum term of ownership of a year, and if you redeem it before five years, you'll forfeit interest from the previous three months. After five years, there is no penalty.

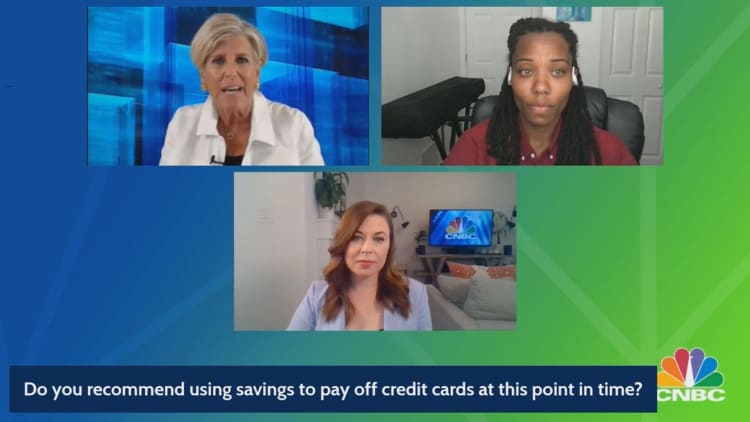

Use savings to pay credit cards?

Kristy Ramsey, owner of Content Maven Media based in Woodlawn, Chicago, wanted to know if she should use her savings to pay down credit card debt.

The answer depends on how much savings would be left over after that debt was paid. Orman recommends having a year's worth of working capital saved for your business, as well as a 12-month emergency fund.

After that, if you have the extra cash, pay off your credit cards, she said.

"When you pay it off, your debt to credit limit ratio goes down and your FICO [credit] score goes up, so when you need a loan you'll get it at better rates," Orman explained.

Investing

Investing should come after you have your emergency fund in place and it should be for the long-term — at least five years and preferably 10 years to 20 years, Orman said.

Protecting those investments from an economic collapse is what worries Denise Merritt, founder and CEO of Apopka, Florida-based Merritt Business Solutions.

Orman's advice: When you have investments, don't freak out when the markets start to go down.

"I don't know one market in all the years I've been doing this that hasn't returned to its peak again," she said.

When to leave your job to start a business

Therapist Catherine Swanson is currently working a 9-to-5 job to pay the bills. However, she really wants to make her part-time business, Alternatives: Music Therapy and Counseling, her full-time job. Her concern is figuring out the best time to do it.

The Ankeny, Iowa-based business currently doesn't make enough money to support Swanson, falling short about $2,000 to $3,000 a month. However, Swanson believes if she goes full-time, she'll make enough.

Before taking the jump, she needs to have a one-year emergency fund in place and about three to four months of working capital set aside for the business, Orman said.

She also suggests getting business credit cards in case Swanson needs a little help — those that don't report to the credit scoring companies. There are some that don't, unless you are delinquent.

"Then, go have a good time and kiss that job goodbye," Orman said.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: 3 side hustle apps that could help you earn money — including one that's 'surprisingly lucrative' via Grow with Acorns+CNBC

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.