Time out of work — either planned or not — can have a major impact on your retirement savings.

In September, there were still 2.7 million Americans who had been unemployed for 27 weeks or more, according to the latest jobs report from the U.S. Bureau of Labor Statistics.

The situation for those who have struggled to re-enter the workforce after a pandemic-related layoff is similar to that of women who decided to take time off to raise children or care for other family members, which also hits retirement savings.

More from Invest in You:

A financial literacy bill would give students $300 to start saving

Majority of states earn a 'C' grade or worse for personal finance education

To combat financial illiteracy, education needs to start early in the classroom

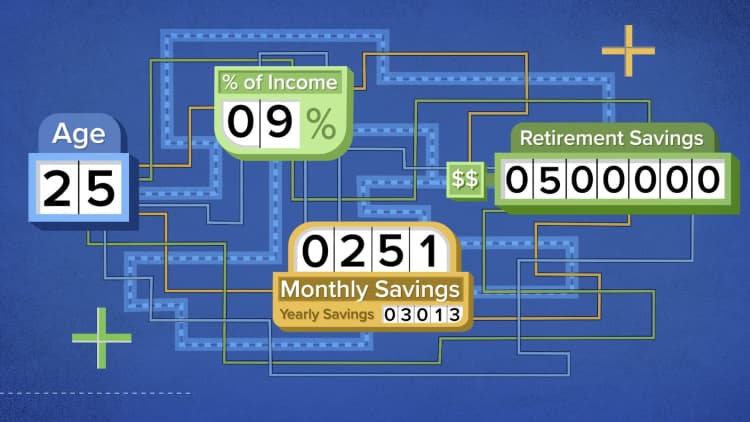

For example, if a 35-year-old woman earning $50,000 annually took a year off of work — and saving for retirement — she'd end up with about $733,125 at age 67, according to a Fidelity survey that assumes she saved 9% of her paycheck with a 3% employer match and a 4.5% real rate of return.

Someone in the same situation who did not take a year off would end up at age 67 with $839,594 in retirement savings, according to the study. That's more than a $100,000 difference from just a one-year break in saving, an amount that increases if you make or save more in a year.

"That doesn't mean that taking a break from work and missing out on participating in a company retirement plan is the end of the world," said Rob Greenman, a certified financial planner and chief growth officer and partner at Vista Capital Partners in Portland, Oregon. "It just means some work needs to be done on coming up with a thoughtful plan on being diligent to getting back on the horse."

How to catch up

If you need to make up for lost time saving for retirement, one of the first things you need to do is get back to work as soon as you can, said Nadine Burns, CFP, president and CEO of A New Path Financial in Ann Arbor, Michigan.

Then, get back to saving as much as you can, to make up for lost time or to replenish your retirement accounts if you had to make a withdrawal due to Covid. Try to put more into an employer-sponsored 401(k) plan than you normally would, such as contributing 15% of your income instead of 10%.

The maximum someone can contribute to a 401(k) plan is $19,500 for the 2021 tax year. Workers over the age of 50 can set aside a total of $26,000 in their 401(k) in 2021, unchanged from 2020.

You can also consider an individual retirement account to save more, such as a Roth IRA, according to Burns. Many Americans are eligible for Roth IRAs — for tax year 2021, single filers must have a modified adjusted income of less than $140,000 annually and married filing jointly income must be $208,000 or less to open and contribute to the account.

Those who are eligible can contribute $6,000 per year if younger than 50.

Older workers can also take advantage of catch-up contributions, especially if they have decided to go back to work. For 2021, you can save an additional $1,000 on top of the regular Roth IRA limits if you're over the age of 50. That means you can sock away $7,000 a year.

Timing also matters

The age at which you have a gap in employment is also important, according to Geoffrey Sanzenbacher, an associate professor of the practice of economics at Boston College and a fellow at the Center for Retirement Research.

Older workers who have been laid off during this recession have been more likely to retire early than try to reenter the workforce, according to data from Center for Retirement Research. That means they may be retiring with less than they anticipated and may draw on Social Security earlier than planned, which lowers the amount they can receive for the rest of their life.

"Every year you claim earlier than you would have, income is 8% lower forever," Sanzenbacher said. This means if you're considering retiring early, you should check whether you have enough saved to hold off on taking Social Security so you don't further cut your income.

On the flipside, the youngest workers who have very little saved — or haven't started saving for retirement at all — can be set back greatly by time out of work. It can mean lower incomes for the rest of your career and missing out on years of compounding interest that would help build a nest-egg long-term.

"It's important that if you have a period where you're not saving that there are times you catch up later on in life," Sanzenbacher said.

People who have a gap in employment in the middle of their careers will still lose out on some retirement saving but will be protected a bit by the money they've already contributed, which will continue to compound in the market.

Ask for help

To be sure, most Americans end up with some gaps in retirement savings, and even with consistent employment may not put away enough to retire when they want.

If you've been out of work and are worried about your long-term savings, working with a financial planner can be a great help to assess where you are and how to get back on track.

"You've got to revisit what your goals are in your plan, and how it's been effected," said CFP Ashley Folkes, financial advisor and director of marketing and growth strategies at Bridgeworth Wealth Management in Birmingham, Alabama.

The earlier you can get a financial plan in place, the better, and it can be helpful at every stage of life, according to Folkes.

"A planner can give you accountability, a second objective opinion and some encouragement to adjust your plan accordingly," he said.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: How to make money with creative side hustles, from people who earn thousands on sites like Etsy and Twitch via Grow with Acorns+CNBC.

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.