Price increases have been challenging for Superfit Hero, an independent plus-sized activewear brand. The Los Angeles-based company typically buys fabric from a local vendor that imports the material from Taiwan, then works with a local factory. But since the pandemic, "the whole process has been disrupted," said Micki Krimmel, the founder and chief executive.

Like many businesses, the company shut operations in spring 2020, but as things reopened, the factory that Superfit Hero was using closed for good. Meanwhile, the price of fabric went up 20%. Krimmel eventually found a new manufacturer, but between higher manufacturing and material costs, prices have tripled since 2019. At the same time, supply chain disruptions meant the company needed to stockpile more material and items to ensure a supply of products for customers

"For small business, having to invest in so much inventory it means our cash flow is tied up. We can't spend on marketing. It's just it's really pressure from all sides," she said.

To ease the pressure, Krimmel applied for the Covid Economic Injury Disaster (EIDL) loan, $150,000 in the first round and half a million in the second round, which the business used to turn things around, stock up on fabric, buy extra inventory and pivot with some new products.

"EIDL is the only reason we're still in business frankly," Krimmel said. With the cash infusion and new products coming, "I am more optimistic now than I was last year," she said.

But the EIDL loan program has ended, while higher costs due to goods inflation, supply chain struggles and rising wages, all remain issues challenging the financial picture for small business owners.

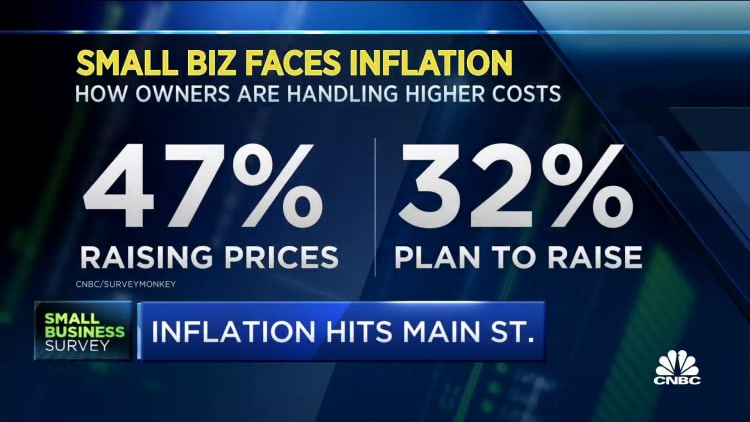

Inflation is at a 40-year high, and in the most recent CNBC|SurveyMonkey Small Business Survey for Q1, 47% of small businesses said they were passing price increases to customers, another 32% indicate they will have to raise prices soon if inflation persists (they think it will), and only 33% described business conditions as good. Other recent surveys from the National Federation of Independent Business and Goldman Sachs have presented a similar portrait of the Main Street outlook in an inflationary economy.

To deal with higher costs, more businesses are taking out loans.

In a survey by the U.S. Chamber of Commerce, nearly half, or 45%, said they have taken out a loan to manage higher costs caused by inflation. According to the SBA, 29.3% of small businesses have sought EIDL loans since May 2020, while 9.5% sought bank loans.

Small businesses historically lean heavily on credit cards or family and friends for capital, said Tom Sullivan, vice president of small business policy at the U.S. Chamber of Commerce, but the pandemic changed that with the Paycheck Protection Program and EIDL loans.

The SBA distributed nearly $416 billion in emergency relief aid to 6 million small businesses through the PPP program, Restaurant Revitalization Fund, EIDL program and other programs in 2021. Now that those programs are over, some expect a turn toward more bank loans.

"Obviously, they got a lot of money over the last two years," said Rohit Arora, chief executive of Biz2Credit, but "now with no other government money coming in, their need for credit is going to grow from here."

The end of government Covid financial relief

Biz2Credit's latest Small Business Lending Index found that loan approval rates increased in January — all kinds of lenders, from big banks to alternative lenders and credit unions are approving more loans though approval rates are still about half of what they were two years ago.

In its latest survey, Goldman Sachs 10,000 Small Businesses found that 48% of small business owners who said inflation was their biggest concern have less than three months of cash reserves on hand.

Small businesses are "going to be turning to banks a little bit higher than they would in the normal historical context. … We're going to see that relationship really, really tested in the next several months," Sullivan said.

The increased appetite for bank loans comes as interest rates are rising, and amid the recent market volatility and sudden flare-up of geopolitical tensions due to Russia's actions in Ukraine, credit markets may tighten.

Most small business lending programs, including the SBA, have floating rates. For businesses that really need a cash infusion, it's also not an ideal time to get a loan because profit and loss statements from the last two years have likely been disrupted by the pandemic, supply chain problems, inflation and higher wages. The Covid EIDL program, besides offering an attractive 3.75% fixed rate, looked at pre-pandemic figures.

"It's basically like a triple whammy. So the storm just keeps kind of getting more complicated and intense. In typical times you would not see businesses use capital to offset macroeconomic conditions," said Joe Wall, national director of the Goldman Sachs 10,000 Small Businesses Voices program. Despite the headwinds, 73% of small businesses said they are optimistic about the financial trajectory of their business in 2022, the Goldman small business survey found.

The EIDL program expired at the end of 2021, but there is hope that Congress might reintroduce it as part of a small relief package targeting small businesses, though policy experts are far from confident about its prospects on Capitol Hill.

What to know about lenders and debt financing

With government lending programs done for the foreseeable future, business owners will need to turn to the usual funding sources. While loan approval rates are still about half of what they were before the pandemic hit in Feb 2020, they are rising in every category of lender, according to the Biz2Credit Small Biz Lending Index.

Here are a few pointers from the small business debt experts on how to navigate the current economy and increase chances of accessing the capital a business may need to grow.

1. Watch your credit score

The last two years have been tough for many small businesses and lower credit scores translate into higher borrowing costs. Businesses, like individuals, also get a score that's affected by payment history, amount of debt, and other factors. But unlike with consumer credit scores, payments to lenders aren't always reported to agencies. Business owners can improve their scores by ensuring their business is incorporated with a federal employer ID, open a business credit card and bank account, and also work with vendors that report payments to business credit bureaus.

2. Get taxes done early

Businesses looking to get a loan soon should make sure their 2021 taxes are completed. Given the influx of government capital in the last couple years via PPP and EIDL loans, most balance sheets are holding up, said Arora, but profit & loss statements are another story. For those with weaker P&L statements, make sure there's a solid explanation for why, said Arora, adding that "most lenders know P&Ls are lower because of Covid."

3. Seek loans from a variety of sources

Banks are major small business lenders, but not necessarily big banks. Community banks fund 60% of small business loans and 80% of agricultural loans, according to Sullivan. "I cannot overstate the importance of these relationships and that is why community banks are so important in the small business finance ecosystem," he said.

Small businesses became more familiar with alternative, digital lenders during the pandemic and may want to consider online options again if more funding is needed. Key Covid financial relief programs like the Paycheck Protection Program included fintech companies in the loan process given the unprecedented volume of loans being made by the SBA, which contributed to greater awareness of fintech as a lending source.

According to a May 2021 report from the New York Fed, fintech lending increased from as little as 2% to as much as 20% of PPP loan amounts during the pandemic, and fintech lenders were most frequently accessed by business owners underserved by the traditional large banking network and lacking existing relationships with lenders. The NY Fed found that fintech lenders approved the highest percentage of applications from Black-owned small employers.

4. Tap free SBA resources and help

Sullivan suggested that small businesses find resources through Small Business Development Centers or find a business mentor through SCORE. Both are public partnerships that don't charge for their services. The Small Business Administration launched a Community Navigator program as a result of Covid to help business owners in underserved communities, including with access to capital.

To learn more and to sign up for CNBC's Small Business Playbook event, click here.