For retirement "super savers," good financial habits appear to go far beyond fattening up their nest eggs, a new study shows.

Most of these workers — whose 401(k) contributions are at least 15% of their pay or 90% or more of the maximum allowed — also pay their bills on time (87%) and don't overdraw their checking account (74%), according to Principal's 2022 Super Saver Survey.

The report, which comes amid raging inflation, rising interest rates and some talk of an economic recession, was based on a recent survey of 1,120 individuals ages 18 to 57 with income ranging from under $35,000 to more than $500,000. All of those surveyed meet Principal's definition of a super saver.

More from Personal Finance:

How to save as food inflation jumps more than 11% in a year

Here's how much you can save by secondhand shopping

Pay isn't keeping up with inflation. What experts say to do

While the idea of becoming a super saver may seem daunting, experts say that small changes in habits and lifestyle can go a long way in helping workers boost contributions.

"I tell people that good money habits aren't too far from good eating habits," said Kathryn Hauer, a certified financial planner with Wilson David Investment Advisors in Aiken, South Carolina.

"You stay the slimmest when you think about every morsel of food you put in your mouth, and you build the most wealth by scrutinizing every penny you part with," Hauer said.

Super savers drive old cars, avoid market worries

Principal asked those surveyed what "sacrifices" they have made to save for retirement. For example, 49% drive an older car, 40% don't travel as much as they'd like and 39% say they own a modest home.

They also have taken steps to shift their money mindset. Many (69%) also don't worry about "keeping up with the Joneses," so to speak, and more than half don't lose sleep over their finances (56%).

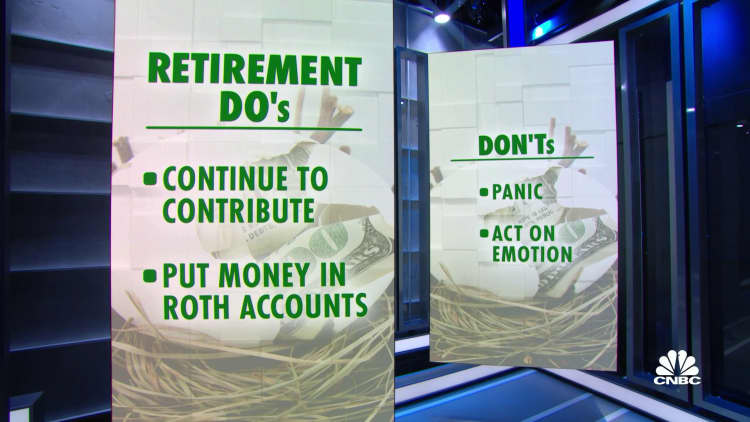

Stock market volatility has not scared off super savers, either: Nearly three-quarters of them consider the current market environment a buying opportunity — one in which they can buy shares at a discount.

This view comes in the midst of the major indexes being down by double digits this year. Through Wednesday's close, the S&P 500 had slid 17.2%, the Dow Jones Industrial Average was off 14.4% and the tech-laden Nasdaq Composite had lost 25%.

Small changes in habits can boost savings

While some households may have little to no wiggle room in their budget to save more for retirement, others may just need to modify their spending to free up more money for long-term savings.

Hauer said that people tend to spend more money when they are in "an intense emotional moment," which can cause decisions that otherwise may not happen.

"It could be at a boutique shopping for the perfect prom dress for your daughter or at the car dealer when you get swept up by exciting extra features on [a car]," Hauer said.

If boosting retirement savings on a regular basis is tricky with your current budget, try stashing away the occasional extra money that comes your way, such as a birthday gift or some of your tax refund.

"Drop surprise cash into a retirement account," Hauer advised.

In 2022, workers can stash a maximum of $20,500 in their 401(k), with those age 50 or older allowed an extra $6,500 in so-called catch-up contributions (for a total of $27,000). For individual retirement accounts, the 2022 contribution limit is $6,000 (with an extra $1,000 allowed as a catch-up amount).