For many Americans, the open enrollment season, which covers both employer-based and federal health insurance, is underway.

Rising health-care costs are a significant cause of stress, and yet, nearly three-quarters of working adults spend 45 minutes or less reviewing their benefits before enrolling, according to recent research by employee benefits provider Unum.

At the very least, workers should evaluate their existing coverage to make sure it is still their best option.

"Look for what's changed, what's new and then what's new with you," said Ashley Shope, the assistant vice president of product development at Unum.

"There are many factors, both in a benefits plan and in one's personal life, that can change every year," Kelley Long, a CPA and member of the AICPA Consumer Financial Education Advocates, said in a statement.

"By 'setting and forgetting' a benefit plan, you not only run the risk of getting stuck in one that isn't right for you but also one that costs you extra."

More from Invest in You:

Here's why you should buy life insurance in your 20s

Here's how to keep health-care costs down in retirement

Don't make this $42,000 mistake

This year, in particular, there could be some changes to the plans that are offered and the details of those offerings, making it even more important to pay attention.

"In general, everybody should go actively through the enrollment process — today more than ever — because the cost and options are radically different than they have been in the past," said David Reid, the CEO of Ease, a benefits administration company.

Here are a few of the things to watch out for:

1. Health insurance

For starters, health insurance is the most significant component of your benefits. Be aware that premiums — and deductibles — are going up.

Annual family premiums for employer-sponsored health insurance — the amount you pay each year for insurance, often divided into 12 monthly payments — rose 5% to over $20,500 this year, according to the 2019 Kaiser Family Foundation Employer Health Benefits survey, while wages rose just over 3% during the same time period.

On average, workers are now paying $6,015 toward the cost of their coverage, while employers pay the rest.

In addition, more workers have a deductible — the amount you pay before coverage kicks in — and that deductible is also rising. The average single deductible is now $1,655 for workers who have one, double what it was a decade ago.

The single biggest issue in health care for most Americans is that their health costs are growing much faster than their wages are.Drew Altmanpresident and CEO of the Kaiser Family Foundation

"The single biggest issue in health care for most Americans is that their health costs are growing much faster than their wages are," Kaiser president and CEO Drew Altman said in a statement.

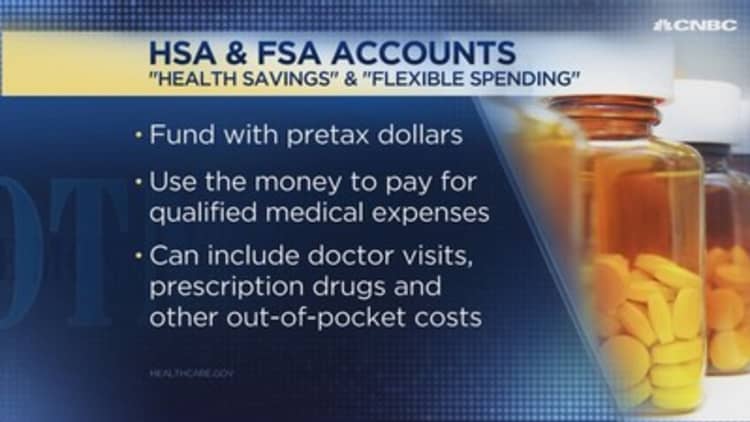

2. Health Savings Accounts

One way to help with health-care costs is by looking for ways to use tax-advantaged accounts for medical expenses. Specifically, health savings accounts (HSAs) or flexible spending accounts (FSAs).

In both cases, you use pretax money to cover out-of-pocket expenses, including doctor visits and prescription drugs.

To be able to use an HSA, you need to be enrolled in what's called high-deductible health plan, or HDHP.

These plans tend to be better suited for people who do not use a lot of preventative health care. The premiums tend to be lower, but the deductibles and the limit on annual out-of-pocket costs are very high.

Because of those high costs, the limit on how much you can save in an HSA is higher, as well. For 2020, employees and employers can contribute a total of up to $3,550 for individual coverage and up to $7,100 for family coverage. (Check to see if your employer offers a flat contribution or matching funds and aim to max out those contributions for the year.)

Contributions then grow on a tax-free basis, and any money you don't use can be rolled over year to year.

FSAs have lower contribution limits — $2,700 for 2019, with limits expected to increase to $2,750 in 2020.

The upside is that you don't need to have a high-deductible plan in order to be eligible for an FSA — in fact, you don't need health coverage at all to sign up for one.

However, you must use the money by year-end or you lose it.

3. Future health-care costs

While you are anticipating your upcoming expenses, it's a good time to think about how your health needs are changing and if you have any big-ticket items on the horizon, such as a planned surgery or braces.

If have a child trying a new sport and you are concerned about possible emergency room visits in the months ahead, then you may also want to consider accident insurance, Reid advised.

There may even be additional options that haven't been available before, according to Reid, such as elder care, which helps cover the cost of care for a qualified adult dependent, or pet insurance.

As it stands, about a third of adults have taken on the role of caregiver, while 22% expect to in the future, one Northwestern Mutual study found.

Of the respondents who already have stepped into that position, nearly half said their new role was unexpected, and often a financial shock.

Try to figure out your future health-care needs, said Myles Ma, a health-care expert at online insurance marketplace Policygenius. "If you don't it could potentially be a costly financial mistake," he said.

4. Changes in your current plan

In addition to the number of employers adding more voluntary benefits, your current benefits could also be different — even if you plan to stick with the status quo.

"It's a constantly evolving landscape," said Unum's Shope.

For example, "your employer could have switched medical carriers or switched plans within your current provider, which could impact your drug plan," she said.

To run through your options and weigh the alternatives, employers often have resources available to enrollees, including online tools.

CHECK OUT: How to get Costco savings without buying the $60 membership via Grow with Acorns+CNBC.

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.