Tax Day is fast approaching.

If you owe the government money and can't pay, don't panic.

There are various options available to you, said Kathy Pickering, chief tax officer with H&R Block.

"Don't freak out," she said. "Take a breath, slow down [and] know that everybody gets into this situation at some point in their lives."

In fact, 37% of taxpayers said they do not have the resources to pay 2019 taxes this year, according to a June survey from TaxAudit. The survey of 1,051 respondents was conducted via SurveyMonkey from May 22 to May 23.

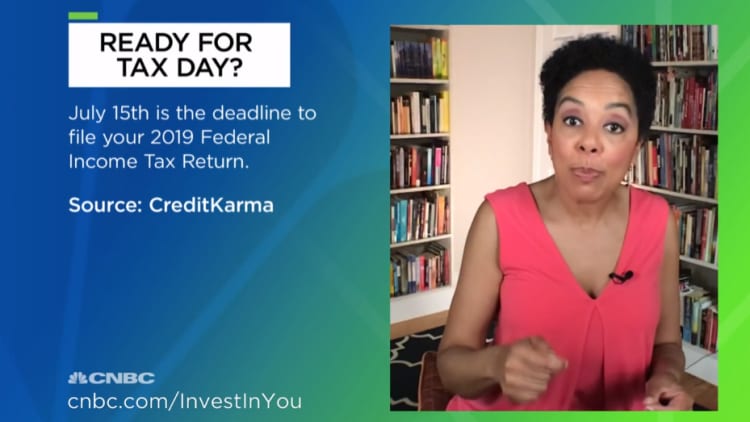

The Treasury Department delayed the April 15 deadline to July 15 this year, giving taxpayers more time to file their federal income tax returns and pay any taxes owed for 2019. However, despite some earlier rumblings, the government opted not to extend it any further.

More from Invest in You:

Tax-saving moves you can still make before the July 15 deadline

Looking to refinance and save money? How to find out if it's right for you

Gig workers are eligible for this $1,000 grant from the government

If you still haven't done your paperwork, you may find the tax bite isn't as bad as you thought it would be.

"A lot of people are surprised to find out how many deductions and credits they are eligible for," said Lisa Greene-Lewis, a CPA and tax expert with TurboTax.

"You may not owe as much as you think."

For example, there is an earned income tax credit for those who qualify, as well as a child tax credit and dependent care expenses credit.

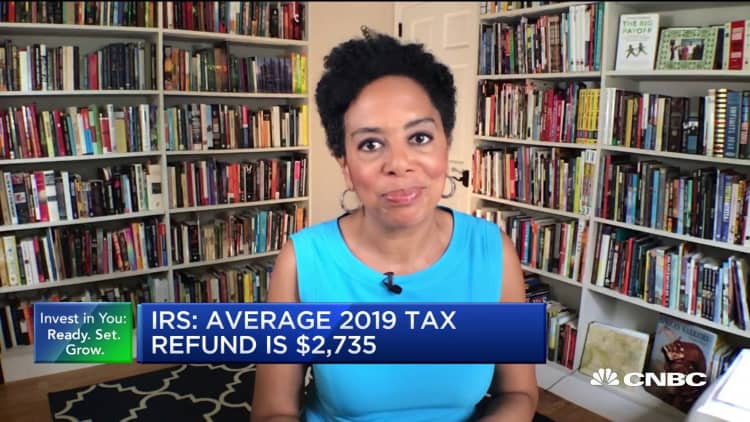

Almost 140 million people had filed their tax returns as of June 26, and the IRS has paid out $259.7 billion in refunds. H&R Block estimates that more than 50% of those who haven't filed yet will be getting a refund.

For those who can't get their paperwork in on time, they can get an extension until Oct. 15. However, if you fail to file and don't seek an extension, you'll be slapped with a penalty of 5% of the unpaid tax you owe.

However, an extension to file doesn't mean an extension to pay. You'll still owe taxes on July 15. If you don't pay, you'll get a 0.5% penalty by the IRS.

"It is far better to file an extension or file a tax return, even if you owe money and can't afford to pay," Pickering said. "You can work out your payment options after that."

It is best to pay off your taxes in full, especially because it will cost you money if you don't.

However, if you can't come up with the funds, go to the IRS website to see what's available and opt for a payment plan. Here are your options.

Short-term payment plan

There is no setup fee for a payment plan of 120 days or less. However, you'll pay accrued penalties and interest until the balance is paid in full.

The IRS can take the payments directly from your checking or savings account, or you can pay by check, money order or debit/credit cards. However, you'll be charged a fee if paying by card.

Installment agreement

If you need more time to pay off your taxes, you can set up monthly payments for up to six years, Greene-Lewis said.

There is a $31 setup fee for automatic withdrawals from your checking account, which is waived for those who qualify as low-income. You'll also pay accrued penalties and interest until the balance is paid off.

Take a breath, slow down [and] know that everybody gets into this situation at some point in their lives.Kathy PickeringH&R Block chief tax officer

If you pay each month and it isn't directly debited from your bank account, you'll pay a $149 setup fee plus penalties and interest. Low income taxpayers are subject to a $43 setup fee that may be reimbursed if certain conditions are met.

To gauge what that might look like, a $5,000 tax bill that was due April 2014 and wasn't paid at all until now would have accrued $1,839 in interest and $1,250 in late payment penalties, for a total balance of $8,079, according to Nathan Rigney, lead research analyst at The Tax Institute at H&R Block.

'Last resort'

If you are facing a large tax bill and won't be able to pay it off, even with paying monthly installments, you may be able to work with the IRS to reduce your payment. It's called an offer in compromise, and isn't as easy to obtain as a payment plan.

Picking called it an "option of last resort."

"If you get into a really bad situation where you are just not going to be able to pay it, then this is a little bit more of a lengthy process," Pickering said.

"You have to, in effect, share some deeper financial information with the IRS to prove that you are unable to pay this."

Also, beware of late-night TV commercials that promise debt relief, she warned.

The IRS considers your ability to pay, your income, your expenses and asset equity when making an eligibility determination.

The agency's website states that it may accept an offer in compromise if there is doubt as to liability (a dispute as to the existence or amount of the correct tax due), doubt as to collectibility (if the taxpayer's assets and income are less than the full amount of the tax liability), or if requiring the payment in full would create an "economic hardship or would be unfair and inequitable because of exceptional circumstances."

If the IRS determines you can't pay any of your taxes, it may temporarily delay collection until your financial condition approves. You'll be charged penalties and interest and the IRS may file a notice of federal tax lien against you.

Other options

If you have the ability to borrow from a family member without paying interest on the loan, that may be an option to pursue instead of an IRS payment plan, Greene-Lewis suggested.

And don't rule out plastic.

If you have available credit, consider using your credit card to pay your taxes, Pickering suggested. However, there are fees involved, which are laid out on the IRS's website. Plus, you'll pay your card's going interest rate on the debt.

Get help

What option you chose will depend on your personal circumstances.

"If you are in the situation where you are a little bit overwhelmed, we would strongly recommend that you work with a tax professional so they can help you navigate through the different options and figure out which is the best for you," Pickering said.

"There is not one answer that is best for everyone."

Fees for a tax professional vary. The average fee for someone to submit your federal and state return with no itemized deductions is $176, according to the National Society of Accountants, but can run up to an average $457 with itemization. For a "simple" tax situation, expect to pay $69 for a federal return and $59 for a state at H&R Block. Prices increase for more complex returns.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: I've been a career coach for 20 years. Here is my best advice for job seekers via Grow with Acorns+CNBC.

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.