Resist the urge to shove your completed 2019 tax return into a drawer. It could help you save money next spring.

Taxpayers and tax professionals were focused on the sprint to July 15 – the new deadline for 2019 federal income tax returns and payments.

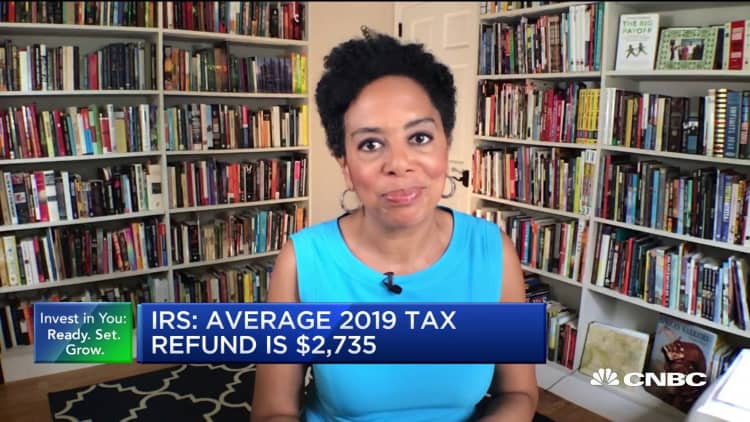

Indeed, the IRS received 147.1 million individual income tax returns as of July 10, the most recent data available. It issued more than 96 million tax refunds, delivering an average check of $2,762.

More from Personal Finance:

Small businesses rehire staff but cut pay and hours

Treasury canceling stimulus checks to dead recipients

Coronavirus unemployment claims are worst in history

Now that you know where you stand with Uncle Sam, it's time to strategize for the remainder of 2020.

"You look at the returns and what things look like for clients," said Albert Campo, CPA and managing partner of AJC Accounting Services in Manalapan, New Jersey. "Were they in a significant deficit position? This is why and this is what needs to change."

Here are four steps you can take to improve your outcomes when you file next spring – and potentially keep a few more of your dollars in your pocket.

1. Review your withholding

A hefty check from Uncle Sam feels good, but the reality is that you're only getting your own money back from the federal government.

Whether you get a huge bill or a generous refund from the IRS, it often comes down to how much income tax you are withholding from your paycheck during the year.

Withhold too much, and you wind up with an oversized refund from the government. The downside is that you'll end up taking home less money.

Withhold too little, and you'll keep more of your paycheck. However, you could end up on the hook for taxes.

Here's another reason to revisit your withholding at work.

The Treasury Department and IRS have overhauled the way income taxes are pulled from your paycheck, bringing in new withholding tables and updating Form W-4, which employees use to tell their employer how much to withhold.

Talk to your tax professional to get a sense of how to best fill out your W-4. The IRS also has a withholding calculator which you can use – along with your tax return – to hash out how much you want to pay Uncle Sam during the year.

2. Boost your workplace savings

Score a win-win for your finances by increasing your contribution to your 401(k) retirement plan at work.

This year, you can stash up to $19,500 in your 401(k), plus $6,500 if you're age 50 and over.

Not only are you shoring up your own retirement nest egg, you're also cutting your tax bill. Money you save in this plan is excluded from your taxable income, which trims your tax load.

Of course, the more you contribute to these accounts, the less you'll be taking home. Make sure you understand how raising these contributions would affect your cash flow.

3. Undo or skip your 2020 RMD

The CARES Act, which went into effect this spring, allowed savers to skip the 2020 required minimum distribution out of retirement accounts.

This is the annual withdrawal you must take from your individual retirement account and 401(k) plans after you turn 70½ — or, starting this year, 72.

If you already took the money, however, you have until Aug. 31 to put it back. This applies to account holders, as well as beneficiaries of inherited IRAs.

Considering RMDs are subject to taxes, waiving a distribution or putting the money back could whittle your tax bill for 2020.

"It's an enormous tax strategy," said Adam Markowitz, enrolled agent at Howard L. Markowitz PA CPA in Leesburg, Florida. "I have to reach out to about 100 to 125 taxpayers and explain to them that they can put the money back."

4. Collecting unemployment? Keep your documents

As more people apply for unemployment benefits, taxpayers must keep in mind the tax ramifications at play.

Any unemployment income you receive must be included in your income for that year. You could have income taxes withheld from your unemployment check by filing Form W-4V.

The other option is to pay quarterly estimated taxes on your unemployment. But you have to be mindful of the deadlines or else face penalties.

Many people don't realize that unemployment is taxable.Neal Stern

July 15 was the deadline for first- and second-quarter payments. The next one is on Sept. 15, followed by Jan. 15.

The government reports your unemployment income on Form 1099-G, which you'll need when you file taxes next year.

"Many people don't realize that unemployment is taxable," said Neal Stern, CPA and member of the American Institute of CPA's national CPA financial literacy commission. "There's a decent chance that it will catch up with you and you'll be stuck with something you really don't want."