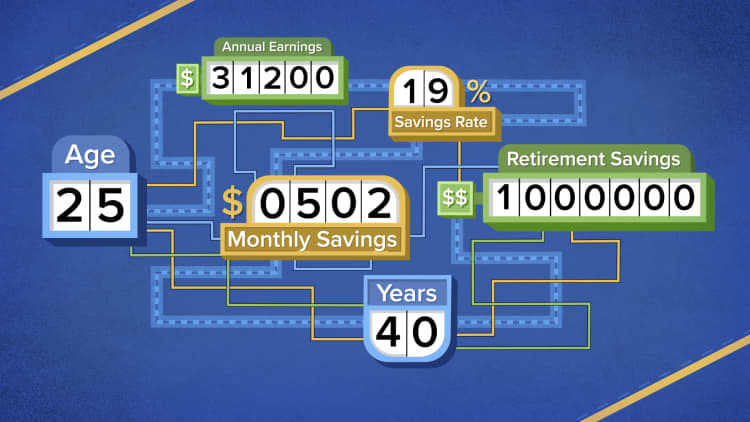

You know you need to save for retirement. Figuring out how to get started or finding the best plan may leave you befuddled.

Yet it is important. By the age of 67, you should have 10 times your final salary set aside, according to Fidelity Investments.

Here are your options, and factors to consider when deciding the best course for your situation.

Employer-sponsored plans

Contributions to a traditional retirement plan sponsored by your employer, typically a 401(k), are automatically deducted through your paycheck, pre-tax. That lowers your taxable income each year. Instead, the tax is taken out when you withdraw the funds in retirement. The rate will therefore depend on your tax bracket at that time.

The big advantage of the 401(k) is that you can save up to $19,500 for 2021, regardless of income, said personal finance expert Chris Hogan, author of "Retire Inspired" and "Everyday Millionaires."

With IRAs, you can only contribute $6,000 this year. If you are age 50 or over, you can save an additional $6,500 in your 401(k) this year or an extra $1,000 in your IRA.

Your company may also offer a Roth 401(k), which means contributions are made after taxes and you won't be levied on retirement withdrawals.

Hogan prefers the Roth 401(k).

"That's putting almost $20,000 away tax-free each year," said Hogan, who is also affiliated with financial education and media firm Ramsey Solutions and hosts an online show, "The Chris Hogan Show."

In fact, a Roth 401(k) essentially allows you to put more money away than a traditional plan, said Pete Hunt, a certified financial planner and director of client services at Exencial Wealth Advisors, based in Charlotte, North Carolina.

Hunt said $19,500 (or $26,000 if over age 50) of after-tax money "is far more valuable than the same dollar amount in pre-tax money, especially over many years."

If your employer matches a certain percentage of your contributions into the 401(k), try to at least contribute up to that match. The company's money will be added pre-tax, whether or not your contributions are taxed.

When you hit age 72, you will have to start taking an annual required minimum distribution, or RMD, from your 401(k), whether you want to or not.

Roth IRA

Contributions to Roth individual retirement accounts also are made after tax, so you don't have to pay taxes when you take money out in retirement.

However, there are income limits. You can contribute the maximum of $6,000 (or $7,000 if you are 50 and over) if you make less than $198,000, if you are married and filing jointly, or less than $125,000 if you are single. You can contribute a reduced amount if you make between $198,000 and $208,000 and are married or between $125,000 and $140,000 if you are single.

More from Invest in You:

Here's a 12-month roadmap to financial wellness

Want a fun way to teach your kids about money? Try these games

Mother of five's budget game plan: Freeze spending for a month

Experts advise building up a Roth IRA when you are young, because you may not qualify when you are older and making more money.

You may also see higher tax rates in the future.

"I recommend it to all my clients, unless they are in a situation where they think they will make significantly less in the future," Hunt said.

There are also no required minimum distribution with Roths and you can withdraw your contributions at any time, tax- and penalty-free. You generally can't tap into any earnings until you reach 59½. You also typically have more investment options than you do in a 401(k).

It also doesn't have to be an either-or situation. If you have a 401(k) but also qualify for a Roth IRA, do both, Hunt said.

First, contribute up to the employer's match for the 401(k). He then recommends putting money in a health savings account, if you have a high-deductible health-care plan. After that, put money into a Roth, which has more flexibility, he said.

IRAs

A traditional IRA is good for those who don't qualify for a Roth IRA or don't have a 401(k). Contributions are made pre-tax, so you'll pay upon withdrawal.

An IRA can also be used to roll over any 401(k) balances from previous employers.

Generally, you should never leave your 401(k) from a previous job with that employer, Hunt said.

You may roll it into your new 401(k) if you are happy with the investment options and want to keep things simple, he said.

However, if the plan has high expense ratios, he advises rolling your old 401(k) into an IRA.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: My side hustles bring in $5,000 a month: Here's my best advice for getting started via Grow with Acorns+CNBC.

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.