People with federal student loan debt have about six more months of freedom from repayment and seeing interest accrue on their outstanding balances.

In the meantime, they can put the money they would be paying towards those loans to work.

The U.S. Department of Education in August extended the moratorium on payment and interest of federal student loans one final time, through Jan. 31, 2022. For millions of borrowers, that means they won't have to make another payment until next February.

More from Invest in You:

10 work-from-home jobs that pay six figures

If you plan to quit, here's what career experts say you should do

Has the 4-day workweek's time come? Some predict it will catch on

"There's a real opportunity for folks to get on good foundations, now that they have a definitive end date in mind, [and] get their financial budgets and households in order," said Robert Humann, chief revenue officer at Credible.com.

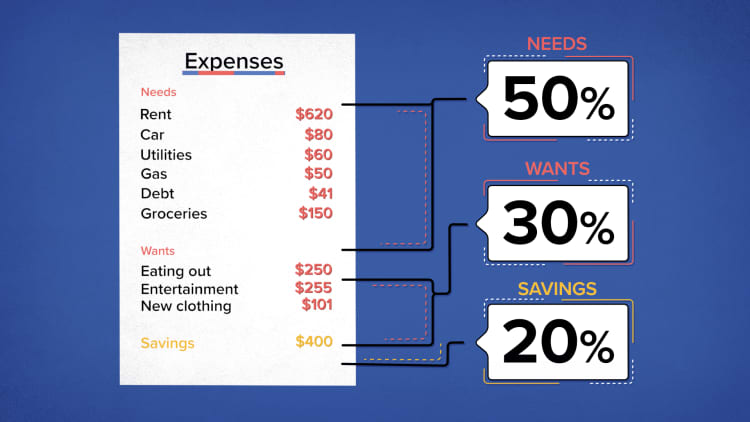

For many Americans, the money they don't need for loans each month could help them make significant financial headway. The average monthly student loan payment is about $400, according to Mark Kantrowitz, a higher education expert.

"It's a matter of understanding what your priorities are and how you can take advantage of these next six months in order to help you hit the fast-forward button on some of those goals," said Lauryn Williams, a certified financial planner and founder of Worth Winning in Dallas.

Boost your savings

If you don't have a solid emergency savings fund, or had to deplete yours during the coronavirus pandemic, it's a good idea to use the extra money from not making student loan payments to build one back up.

Generally, experts recommend having between three months to six months of living expenses put away in cash. But, after the health crisis, some people may want to save even more.

Reallocating the money from student loans could help people put a solid chunk of cash away quickly. For example, if your monthly student loan payment was $400 — roughly the average — and you save all of it, you could have $2,400 between now and February.

Pay down other high-interest debt

Paying down debt is another great way to better your financial situation over the next six months, before payments resume.

If you have high-interest debt such as credit cards, see if you could pay off the balance or at least make significant progress over the next half year.

"Focus on paying that down as much as you can," said Humann. "That can help you minimize the interest that you're going to pay and save you more money over time."

Even if you don't completely wipe away the debt, any progress will be a benefit to you in the long run, according to Humann.

Invest it

If you have savings you are happy with and don't have to pay down any other debt, you can look at investing the additional money, according to financial advisor Delano Saporu, CEO and founder of New York-based New Street Advisors Group.

The more money you have compounding, the better.Delano SaporuCEO of New Street Advisors Group

If you're new to investing, that means opening a brokerage account or potentially a Roth individual retirement account, which has certain tax and trading advantages. Investing your extra money helps it grow over time, and can mean you meet longer-term savings goals faster, such as having enough for a down payment on a house, a wedding or even to retire.

Even putting a small amount into the market now will help you in the long run, according to Saporu.

"The more money you have compounding, the better," he said.

Reassess repayment options

As you're working towards other financial goals, another thing student loan borrowers should do before payments resume in February is review their budget and repayment plan. Things may have shifted a lot since the last time you made a payment, especially if you had a change in employment due to the pandemic.

"This is a great time to check in and make sure that the payment strategy you're using is the optimal one for your personal finance situation," said Williams.

That means looking at what your monthly payment will be when come February, if you can afford it, and if not, what other repayment options are available. Questions can be directed to an expert such as a financial planner, professional student loan consultant or your student loan servicer.

Refinance private loans

Many Americans have both public and private student loans, which generally require different repayment strategies. While federal loans have been paused, most private loans have not been put on hold.

Still, now may be a good time to consider refinancing a private student loan because interest rates are so low, experts say. Having a lower interest rate on such loans could save you a lot of money over time.

To be sure, this does not apply to most people with public student loans, which should not be refinanced at this time.

That's because when you refinance a public loan, it becomes a private one and is thus no longer eligible for certain programs such as the current pause on payments and interest. It also means borrowers can't enroll in different repayment plans or get certain types of loan forgiveness.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: How to make money with creative side hustles, from people who earn thousands on sites like Etsy and Twitch via Grow with Acorns+CNBC.

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.