If you didn't put the maximum amount of money into an individual retirement account or health savings account last year, you still have about one month to do so for 2021.

The deadline for 2021 contributions is April 18, 2022, the same day individual tax returns are due.

For those who can afford it, saving for a previous tax year in these accounts makes a lot of sense.

"You always want to take advantage if you have the money," said Ed Slott, CPA and founder of Ed Slott and Company.

More from Invest in You:

Want to give your finances a spring cleaning? First, get organized

Here's what to know about managing your debt in retirement

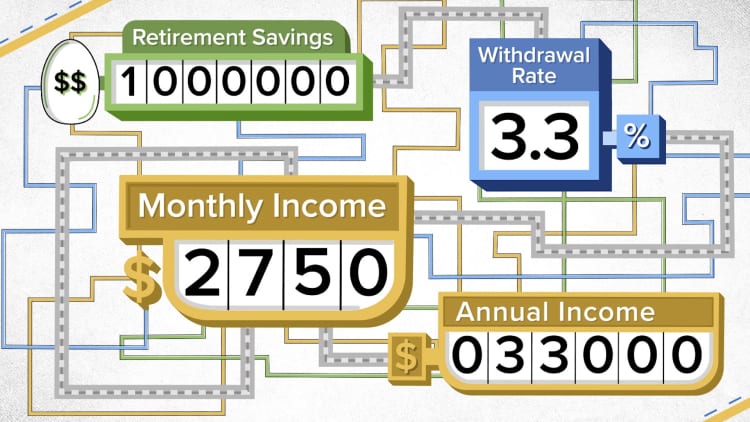

Want to find financial success? Here's how to get started

Invest in an IRA

One place where you can contribute now and have it count it towards the 2021 tax year is an IRA. These accounts allow people to save outside of employer-sponsored 401(k) or 403(b) plans.

People with earned income can contribute up to $6,000 in a traditional or Roth IRA for 2021. Taxpayers who are 50 or older can sock away $7,000 in the same accounts as a catch-up contribution.

Putting money into an IRA for the 2021 tax year can help you catch up if you're behind on retirement savings or would like to have a larger cushion set aside.

Say, for example, you're 40 and have $10,000 to invest, but you put only $2,000 in a Roth IRA for 2021. This year, you could put an additional $4,000 into the account for 2021, making the maximum contribution. Then, you could invest the rest of the money — $6,000 — into the account for 2022.

There's an additional benefit to investing in a Roth IRA: The money you contribute is post-tax, meaning you won't be hit with taxes when you withdraw the money come retirement.

"That's the best starting point, especially for younger investors," said Christine Benz, director of personal finance at Morningstar.

"You're planting seeds for trees that will grow much later, and you want those trees to produce benefits to you that are tax-free," said Slott.

Fund a health savings account

Another place to put extra money for the 2021 tax year is an HSA.

Generally, people who are eligible for such accounts are covered under a high-deductible health plan.

For 2021, the contribution limit for HSAs is $3,600 for individuals and $7,200 for families. If you're 55 or older, you can contribute an additional $1,000 as a catch-up.

HSAs are popular because they come with a triple tax advantage. People contribute pre-tax dollars to the accounts, the money grows tax-free and withdrawals used for qualified health-care expenses are also untaxed.

"HSAs are the most attractive vehicle from a tax standpoint," said Benz.

In addition, unlike other types of saving accounts, money in HSAs can be rolled over at the end of the year, so it's not a "use it or lose it" situation.

And, though you generally set contributions through your payroll withholdings, you can change the amount throughout the year.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox. For the Spanish version Dinero 101, click here.

CHECK OUT: 74-year-old retiree is now a model: 'You don't have to fade into the background' with Acorns+CNBC

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.