For some young adults, having a full-time job doesn't translate into financial independence from their parents.

Nearly a quarter (24 percent) of millennials who are fully employed report receiving help from their parents with bill-paying, according to a recent survey by Instamotor.com. The majority of them, about 80 percent, do not live with mom or dad.

"For some millennials, especially those just transitioning into adulthood, it can take some time to get to the point where they don't need their parents' help," said certified financial planner Marguerita Cheng, CEO of Blue Ocean Global Wealth in Gaithersburg, Maryland.

"I'd never tell a parent not to help their kids, but they do need to set parameters," Cheng said.

The Instamotor survey polled 800 millennials — defined as ages 18 through 34 — who are working 35 hours or more week. The most common bills picked up by parents are those for cellphones (53 percent) and car insurance (31 percent).

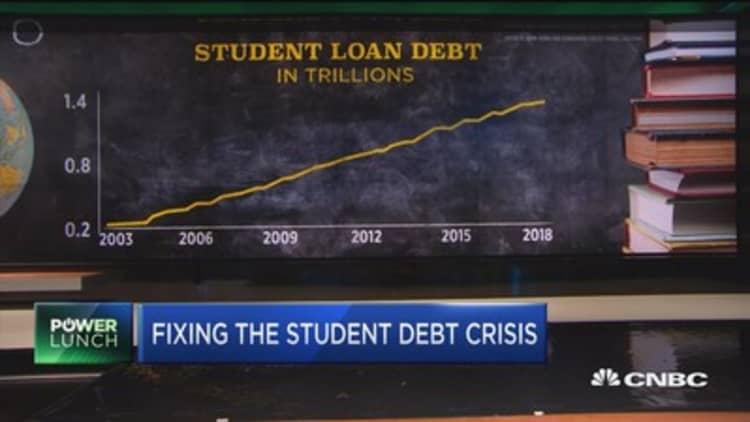

The largest and most diverse generation at 75.4 million strong, millennials generally face financial challenges that their parents did not as young adults. On top of carrying most of the $1.4 trillion in student loan debt, their wages are lower than their parents' earnings when they were in their 20s.

A 2017 study of Federal Reserve data by advocacy group Young Invincibles showed that millennials earned an average of $40,581 in 2013. That's 20 percent less than the inflation-adjusted $50,910 earned baby boomers in 1989.

If you take into consideration all adult children — those age 18 or older who may or may not be working full time — the reliance on parental support broadens significantly. A 2017 study from CreditCards.com found that 74 percent of parents reported helping adult kids with expenses and debt.

While financial independence might take longer to reach for some millennials than for previous generations, there are a few considerations for those who turn to their parents for support.

Be transparent

Entering adulthood generally provides more privacy and independence from your parents, but that changes if you ask them for money.

"Once you ask for financial help, your business becomes your parents' business," Cheng said. "I'm not saying you need to share everything, but you can't just ask people to give you money without letting them understanding the situation and why you need financial help."

Get a handle on your budget

If overspending is causing the reliance on parents, scrutinize where you can cut back.

Research from Slickdeals.net shows that impulse purchases set the average consumer back $5,400 yearly. The biggest category for spur-of-the-moment purchases? Food. Entertainment also has a way of eating up more cash than intended.

For those whose spending habits are in line with their means, other parts of your budget could possibly be trimmed. For instance, perhaps cheaper car insurance is available, or maybe you can reduce your living expenses by having a roommate split the rent and utilities.

If you are repaying a student loan and the monthly payments are burdensome, ask your lender if you can lower your bill.

For example, borrowers who earn below a certain threshold might qualify for an income-based repayment plan for federal student loans. This would let you pay a percentage of your income rather than a flat rate.

While private lenders operate under different regulations, they might be willing to work with you to make your loan more affordable.

"Find out your options if you're having problems making your payments," Cheng said. "Asking what you can do doesn't hurt, but not sending the payment or full payment could mess up your credit."

Have an exit strategy

You should have a sense of when you can take over the bill (or bills) that your parents are paying for you. Whether it's a matter of months or years, there should be an agreement on when the reliance will eventually end.

"Becoming self-sufficient is a reasonable goal," Cheng said. "But it can take time. I don't think parents can go from providing 100 percent support to cutting off kids overnight."

Remember, too, that some parents are prone to letting themselves suffer to help their kids. If their retirement nest egg is at risk, or they are going into debt to help you, that serves no one's best interest.

"If parents are helping the child to the point it affects their retirement savings, that's not good," Cheng said. "They shouldn't be supporting them at the expense of their own [financial security]."

More from Personal Finance:

Your retirement plan is getting a facelift. How to take advantage

Are you considering an adjustable rate mortgage? Here are the pros and cons

How to clean up financial clutter