Women face a unique set of challenges when it comes to retirement planning.

Unfortunately, research shows female workers are coming up short compared to their male counterparts.

The good news is there is room for women workers to take steps now to improve their prospects for a better-quality retirement, according to Catherine Collinson, CEO and president of Transamerica Institute and Transamerica Center for Retirement Studies.

"Our research consistently finds action steps that are within reach for most women, and they may even seem somewhat basic," she said, starting with saving and budgeting. "But many women are not yet doing them."

To be sure, men are guilty of not taking some of these steps, too. But women fall short to a larger degree, she said.

Women workers have less than half of the total household retirement savings than men do, with an estimated median of $57,000 versus $118,000, a recent report from Transamerica Center for Retirement Studies found.

Women are less likely than men to have $250,000 or more saved in total household retirement accounts, with 24% versus 35%.

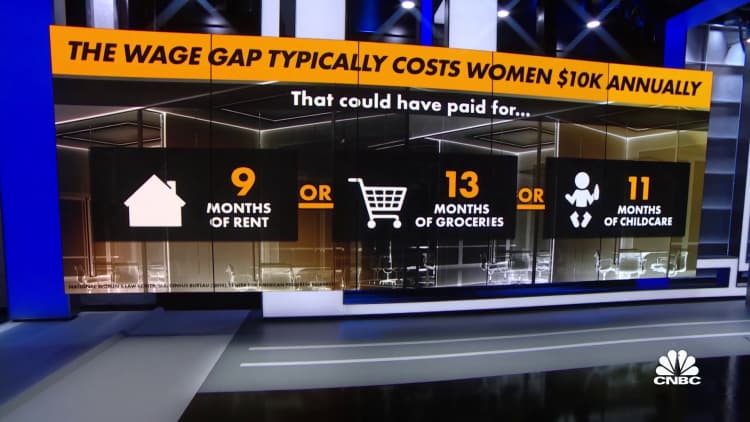

Notably, 24% of women and 14% of men have less than $10,000 saved or nothing at all. Women are paid 83 cents for every dollar men earn. And that gap is even bigger for women of color.

"The gender pay gap leads to an even greater retirement savings gap," Collinson said.

Moreover, women also confront unique challenges when it comes to planning for their non-working years. For one, they tend to live longer than men.

Additionally, they are more likely to take time out of the work force to care for children or loved ones. That can lead to reduced retirement savings and eventually less in Social Security benefits based on their own work record.

For female workers, having access to a retirement plan at work is key to boosting their retirement savings.

Look for new employment

Abundant job opportunities may help women rejoin the work force or find better-paying opportunities.

Available job openings hit a record 11.55 million in March, according to the latest government data.

"Employers are looking for talent, so for women who are ready to jump back in, now is a great time to do so," Collinson said.

Finding a more lucrative position may be a first step toward improving retirement security, particularly if there is an employer match on 401(k) plan contributions.

Admittedly, women who have taken on caregiving responsibilities may not be able to work full time. But they may want to consider taking on part-time or contract work if they're able to. That can help reduce their need to dip into savings, and also help pave the way for them to return to the work force when they're ready, Collinson said.

Engage in planning

"Many women are saving for retirement, but they have not yet started engaging in financial planning," Collinson said.

That may start with simply talking more about retirement, Collinson said.

About 28% of women never talk about retirement, versus 17% of men, according to Transamerica. Moreover, just 17% of women frequently discuss saving, investing and retirement planning, compared to 28% of men.

Stay involved in family finances

Women in the work force are much more likely than men to say they're not familiar with their spouse's or partner's retirement savings.

But women should not hesitate to get more involved in all aspects of their family's financial planning, Collinson said.

"In a marriage or partnership, it's a partnership. Both parties should be equally engaged in the household finances," Collinson said.