We are three weeks into the new tax season and average tax refunds continue to be lower than last year.

The average tax refund is $2,640 for the week ending Feb. 15, according to the IRS. That's down by more than 16 percent compared to the year-ago period.

For the first time, taxpayers are submitting their returns under the Tax Cuts and Jobs Act, which went into effect last year.

The filing season only kicked off on Jan. 28, but some early filers are finding that they're either owing the IRS or they'll be receiving a smaller refund.

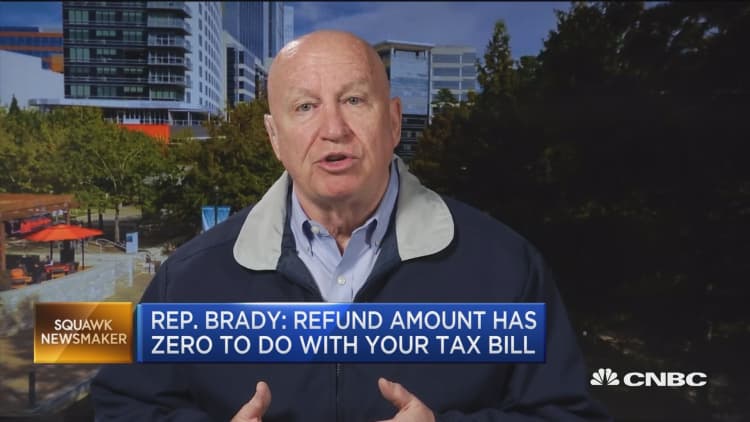

Rep. Kevin Brady (R-Texas), who sponsored the tax overhaul as it made its way through Congress, told CNBC on Thursday that filers' refunds are smaller for 2018 because they got their money in their paychecks.

He said filers can retool their tax withholding at work using Form W-4.

"People can go at work, fine-tune how much they want in their weekly or monthly paycheck and what they want in their refund," Brady told CNBC.

If you withhold too much, you're likely to get a refund.

However, if you withhold less, you'll see more cash in your paycheck in the immediate term. But the following year, your refund will be smaller — or you may owe if you withhold far too little.

"The people who are most likely to be surprised this year are the ones who lost some deductions they had last year and who didn't make changes to their withholding," said Nathan Rigney, lead tax research analyst at the Tax Institute at H&R Block.

Withholding review

In 2018, the Treasury Department and the IRS updated the withholding tables to reflect the new Tax Cuts and Jobs Act.

Major changes from the new law include the end of personal exemptions, the doubling of the standard deduction, and reduced individual income tax rates.

These withholding tables are guidelines that your employer follows in order to deduct the right amount of income tax from your paycheck.

Everyone wants to know, 'Did I save money or not with the new tax bill,' and the best way to check is to look at liability versus income.Chris BensonCPA and principal at L.K. Benson & Co.

The tables are intended to work alongside Form W-4, which you can use to tailor your taxes based on whether your spouse works, whether you have children and other factors.

The tax agency has been reminding taxpayers through 2018 to take a second look at their withholding and make estimated payments, if needed.

Even retirees were encouraged to ensure they were withholding sufficient tax from pension and Social Security payments.

Last month, the IRS announced it would waive the estimated tax penalty for filers who paid at least 85 percent of what they owed during 2018.

Normally, you have to pay at least 90 percent of your tax liability in order to avoid the penalty.

If you owe this season, consider it a lesson learned and do what you can to head off the same troubles in 2019.

It's generally a good practice to review your withholding, especially if you've been through major life changes, including getting married or having children.

Some taxpayers should pay even closer attention to their W-4s:

• W-2 employees with side gigs: Got a side job in addition to your 9-to-5? Odds are that you aren't withholding enough in taxes to cover both streams of income.

"If you're not making estimated tax payments for your side job, then there's a good chance you'll owe taxes," said Rigney.

• Itemizers: Under the old tax law, people who itemized their tax returns may have withheld less tax from their pay.

However, fewer people are expected to itemize under the new tax law, so they should review their W-4s.

That's because the standard deduction has been nearly doubled to $12,000 for singles and $24,000 for married couples who file jointly (2018).

• Families with dependents: Previously, it may have made sense for families to have less tax withheld from their pay if they had dependents.

However, the new tax law has done away with personal and dependent exemptions. It also broadened the applicability of the child tax credit to include higher-income households.

If you haven't already made these updates to your withholding and you owed for 2018, be sure to review your W-4.

• Retirees: You may have stopped punching in at work, but you still need to reevaluate your withholding. Use Form W-4V to withhold a flat rate from your Social Security check or Form W-4P to withhold from your pension.

Avoid surprises next year

CPAs are helping clients manage their expectations this tax season.

If you're unhappy with your 2018 results, talk to your tax preparer or accountant about running a projection of your 2019 taxes so that you can head off any surprises.

Also, don't get too tied up in your tax refund as a chief determinant of how you fared this tax season.

Instead, look at your tax liability last year versus this year and see how they stand against your income, said Chris Benson, CPA and principal at L.K. Benson & Co. in Towson, Maryland.

"You want to compare the tax liability to your income," he said. "Everyone wants to know, 'Did I save money or not with the new tax bill,' and the best way to check is to look at liability versus income."

More from Smart Tax Planning:

Why secret cash payments to your nanny could backfire

Getting zero back from the IRS might be a good thing

Five ways to jump-start your tax return