Many Americans are grappling with what to do with their retirement savings, uncertain whether to head for the exits or buy more stocks on sale. The recently passed CARES Act makes it easier for you to tap your 401(k) and retirement accounts, but there could be significant long-term consequences for your financial security. I spoke with several financial experts to get answers to your most pressing concerns.

My 401(k) has dropped $31,000 in three weeks. Should I borrow some now to prevent bigger losses?

You're not alone in thinking about tapping your 401(k) right now. A survey earlier this week by Blind -- an anonymous professional network of about 3.5 million verified workers, mostly in technology and financial services industries -- found that 48.5% of the 3,800 respondents have made changes in their 401(k) account since the start of the coronavirus pandemic.

While 25% contributed more or increased their investment and 11% contributed less or decreased their investment, nearly 6% said they withdrew money from their retirement plan or divested stock options, if they had them. Blind conducted another survey on Friday that found about 3% had taken out a 401(k) loan in the past month, while nearly 8% withdrew cash from their workplace retirement plan.

If you need emergency cash and your 401(k) is your only source of funds at this unprecedented time, then taking a short-term loan from your retirement account as a "last resort" may be a viable option, some financial advisors say. You'll be paying yourself back instead of paying 11% interest on average on a personal loan. However, keep in mind you're borrowing from your financial future and possibly jeopardizing your financial security in retirement.

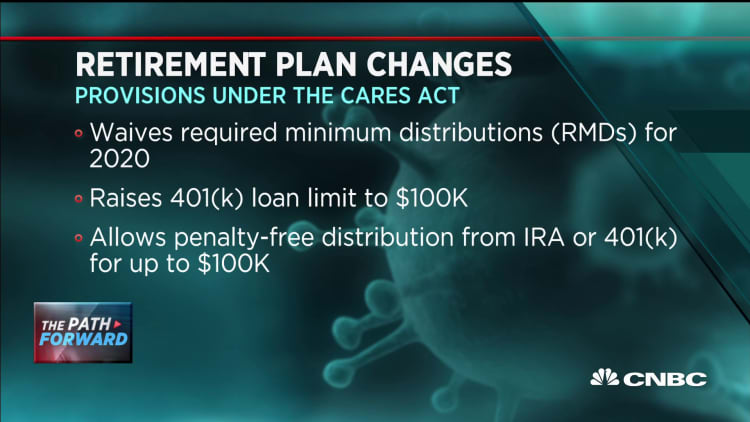

The recently passed CARES Act now allows you to borrow up to $100,000 (previous loan limit was $50,000) from your 401(k) and delay repayment for up to one year. After you borrow, you'll typically have to repay the loan within five years, depending on the terms of your 401(k) plan. Under the CARES Act, loan payments due in 2020 can be delayed for up to one year from the time you take out the loan. However, if you can't pay back the loan within the time frame designated by your plan, your outstanding balance will be taxed like a withdrawal, and you'll also have pay a 10% early withdrawal penalty.

It's also important to note that if you leave your job — whether by choice or not — there's a good chance your plan will require you to repay the money back fairly quickly; otherwise, your account balance will be reduced by the amount owed and considered a distribution. And unless you are able to come up with that amount and put it in a qualifying retirement account, that distribution is taxable. ·

According to certified financial planner Carolyn McClanahan of Life Planning Partners in Jacksonville, Florida, "borrowing against a 401(k) to prevent losses is not a good idea." Taking money out of your retirement savings account when the market has fallen means you're locking in your investment losses, she says. Now is the time to review and reassess your asset allocation.

This choice depends on how long before you need your money, your ability to save, and your psychological ability to take risk.Carolyn McClanahancertified financial planner and director of financial planning at Life Planning Partners

"The best action is to create an investment policy to determine how much they should have allocated to risky assets and to safe assets," said McClanahan, who is also a member of the CNBC Financial Advisors Council. "How much risk to take depends on your time horizon, ability to save and psychological ability to take risk. Once an investment policy is created, assets should be rebalanced to fit the investment policy."

If you need to take cash out of your 401(k) due to financial hardship caused by the coronavirus pandemic, the recently passed CARES Act now allows you to borrow up to $100,000 (previous loan limit was $50,000) from your 401(k) and delay repayment for up to one year. You could also take a penalty-free distribution from your IRA or 401(k) of up to 100% of your balance or $100,000, whichever is less. You won't have to pay the 10% early withdrawal penalty if you're under age 59 ½ — and you can pay taxes on the money you take out over a period of three years or pay no tax if you pay it all back. The catch is that your employer has to agree to adopt these new provisions for your existing 401(k) plan.

Since the new law passed just a few weeks ago, some employers are still deciding whether to change their plans to include these provisions. Yet retirement plan consultant Denise Appleby says that "if enough employees show interest, some employers, who were unwilling, might determine that it is worth the administrative costs for handling the transactions and amending the plan."

We are 62 and 67. Should we move our 401(k) money into a Roth IRA, as we do not have longevity to recover huge losses due to coronavirus? We want to have access to the money with least penalties.

Since you're both in your 60s, if you want to move your 401(k) money to a Roth IRA so that you can take out that money penalty-free, you don't have to make a move at all. The 10% early withdrawal penalty applies to 401(k) account owners who are under age 59 ½, so you would not be penalized for taking money out. However, you will have to pay taxes as you withdraw the 401(k) money. With a Roth IRA, you can make tax-free withdrawals.

One option is to withdraw your 401(k) over time to reduce the tax hit, McClanahan said. Another option is to do a 401(k) rollover into a traditional IRA. "Often, workplace 401(k)s charge fees to make withdrawals, plus you often have to go through an administrator to get distributions. IRAs at self-directed brokerages don't have these types of issues," she said. The third option is rolling all of the 401(k) money into a Roth IRA. Just keep in mind, you'll "have to pay taxes on the entire conversion in one year, which can be pretty hefty," McClanahan said.

More from Invest in You:

You really should resist the siren call of cashing out your 401(k)

If you think your job is on the chopping block, here's what to do

This simple financial plan makes it easier to get through tough times

On the other hand, now may be a really good time to consider a conversion, since investment values are lower and you may pay less in tax to convert to a Roth IRA, said certified financial planner Diahann Lassus of Lassus Wherley and a member of the CNBC Financial Advisors Council.

"If you are unsure whether you may need the money but the tax rate is low, then consider that minimum distributions are not required from Roth accounts. This means the money can grow tax free perhaps for a longer period of time. And if you do need it, you may take only what you need tax free," she wrote in a recent newsletter to clients.

You have several options for the type of account where you put your retirement savings, but where you invest that money is also extremely important. "My bigger concern is that they are too aggressively invested if they had huge losses," McClanahan said. "They should consider consulting a financial planner to help them determine if they should change their investment allocation and to determine what type of account would be best for them going forward."

In response to the coronavirus pandemic, many financial advisors around the country are offering their services at reduced rates or for free to those in need. Look for an advisor in your area by going to the Financial Planning Association and National Association of Personal Financial Advisors' websites.

I'd like to buy some stocks during this downturn in the market. I know if I choose right, it could really make my retirement comfortable. What are some good choices?

"Picking individual stocks is a guessing game. The best way to invest is to buy low cost, well-diversified mutual funds or ETFs that are invested in a broad basket of stocks," McClanahan said. You can Google mutual funds or exchange-traded funds (ETFs) you may be interested in or go to Morningstar, an investment research firm, to find out about a fund's fees, performance over time and what companies, sectors, stocks and/or bonds make up the fund. Morningstar also provides a star rating for each investment's performance.

However, "the most important decision to make is your asset allocation," McClanahan said. "How much should you have invested in risky assets such as stocks and stock funds and how much should be invested in safer assets, such as bonds and bond funds? This choice depends on how long before you need your money, your ability to save, and your psychological ability to take risk."

ASK QUESTIONS: Managing your money in the middle of a pandemic is an unprecedented dilemma. Submit your money questions; Sharon Epperson will turn to experts for the answers.

TUNE IN: CNBC 7 p.m. tonight for more insight from Carolyn McClanahan on managing your money through this crisis.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: How to use your stimulus check to invest for the future via Grow with Acorns+CNBC.

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.